If you are planning to start investing in India, one term you will hear everywhere is what is SIP.

Mutual fund platforms promote it.

Financial advisors recommend it.

Most salaried professionals rely on it to build long-term wealth.

But what is SIP?

Is it safe?

How much return can you expect?

And how does SIP actually help you build wealth over time?

Many beginners think SIP is a special investment product.

It is not.

SIP is simply a method of investing small amounts regularly into mutual funds so you can build wealth without worrying about market timing.

If you are completely new to investing, first read our complete beginner roadmap here:

👉 Start Investing in India

In this detailed guide, you will learn:

- What SIP really means

- How SIP works step by step

- Types of SIP in India

- Expected returns from SIP

- SIP vs Lump Sum and FD

- Who should invest in SIP

- Common SIP mistakes

- How to start SIP today

By the end of this guide, you will clearly understand whether SIP is right for you.

What is SIP?

SIP stands for Systematic Investment Plan.

It is a facility offered by mutual funds that allows you to invest a fixed amount at regular intervals — usually monthly.

Instead of investing ₹60,000 at once, you can invest ₹5,000 every month.

The amount gets automatically deducted from your bank account and invested in a selected mutual fund.

That’s SIP.

It is not a separate investment product.

It is a disciplined way of investing.

Think of SIP like a recurring deposit — but instead of fixed interest, your money is invested in market-linked assets like equity or debt mutual funds.

How SIP Works (Step-by-Step Explanation)

Let’s understand how SIP works in simple terms.

Step 1: Choose a Mutual Fund

You select a mutual fund — for example:

- Nifty 50 Index Fund

- Large-cap mutual fund

- Flexi-cap fund

Step 2: Decide Monthly Amount

You choose how much you want to invest:

₹500

₹1,000

₹5,000

₹10,000 or more

Step 3: Select SIP Date

You pick a date — for example 5th of every month.

Step 4: Set Auto-Debit Mandate

Your bank account is linked.

The money gets automatically deducted every month.

Step 5: Units Are Purchased

Based on the fund’s current NAV (Net Asset Value), you receive mutual fund units.

If NAV is high → you get fewer units.

If NAV is low → you get more units.

Over time, this balances your average cost.

This process continues automatically until you stop the SIP.

Why SIP is So Popular in India

SIP has become extremely popular among Indian investors for three major reasons.

1. You Don’t Need Large Capital

You can start SIP with as little as ₹500 per month.

This makes investing accessible to:

- Students

- Fresh job holders

- Salaried professionals

- First-time investors

You don’t need lakhs to begin.

2. It Removes Market Timing Stress

Most beginners are afraid of investing because they think:

“What if I invest at the wrong time?”

With SIP, you don’t worry about timing.

You invest regularly.

When markets fall → you buy more units.

When markets rise → you buy fewer units.

This is called rupee cost averaging.

It reduces the risk of investing at a bad time.

3. It Builds Investing Discipline

SIP works automatically.

Just like:

Rent

EMI

Utility bills

Your investment also becomes a fixed monthly commitment.

This discipline is what builds long-term wealth.

Power of Compounding in SIP (How Wealth Actually Builds)

The real magic of SIP is not high returns.

It is compounding.

Compounding means your investment returns start generating their own returns over time.

In simple words, your money starts earning money.

And then that money also starts earning.

This snowball effect is what builds long-term wealth.

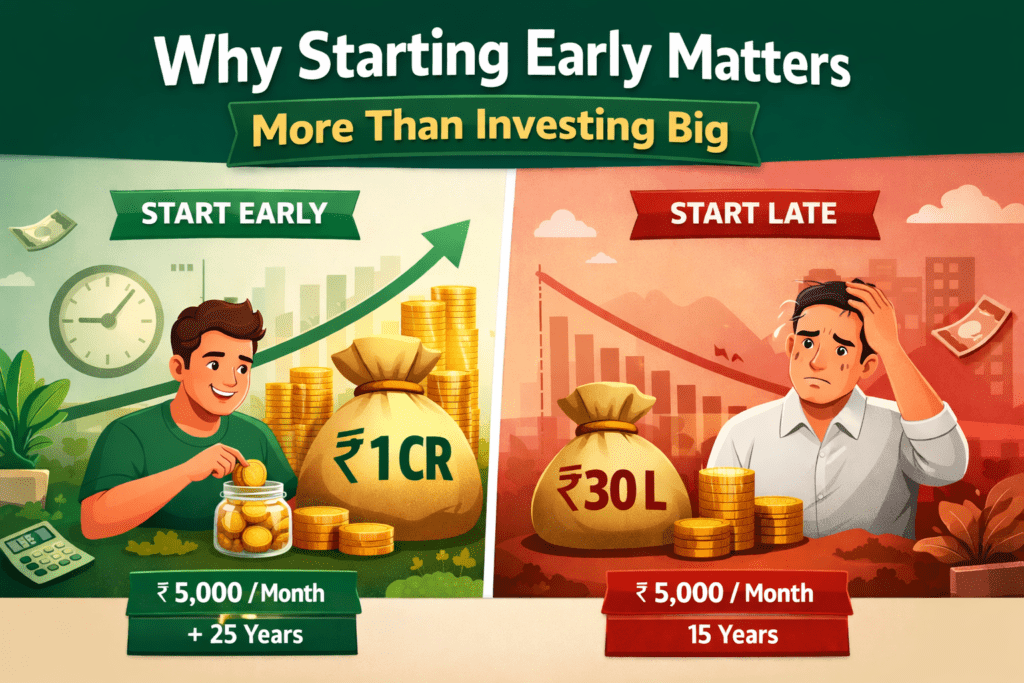

Why Starting Early Matters More Than Investing Big

Many people delay investing because they think they need a large amount.

That’s not true.

Time is more powerful than amount.

Let’s understand with a simple example.

Example 1: Starting Early

If you invest ₹5,000 per month from age 25

for 25 years at 12% average return:

You could build a corpus of over ₹95 lakhs to ₹1 crore.

Example 2: Starting Late

If you start at age 35

and invest ₹5,000 per month for 15 years:

You may build only around ₹25–30 lakhs.

Even though you invested the same monthly amount,

starting 10 years earlier created a massive difference.

That is the power of compounding.

SIP Works Best With Time

SIP is not a shortcut to quick money.

It is a long-term wealth creation strategy.

The longer you stay invested:

- The stronger compounding becomes

- The less market fluctuations matter

- The more stable your growth becomes

This is why most successful investors stay invested for 10–20 years or more.

Small Amounts Can Become Big

Many beginners think:

“₹1,000 or ₹2,000 SIP won’t matter.”

But consistency matters more than amount.

Even a small SIP, increased gradually every year, can grow into a significant corpus over time.

👉 Check our SIP and Lump Sum Calculator

You can also increase your SIP whenever your salary increases.

This is called a step-up SIP and it accelerates wealth creation.

The goal is simple:

Start early.

Stay consistent.

Increase over time.

That’s how compounding works in your favour.

Types of SIP in India You Should Know

Most beginners think SIP has only one format.

But there are actually multiple types of SIP available in India.

Understanding them helps you choose the right strategy based on your income and goals.

Let’s go through the main types in simple terms.

1. Regular SIP (Most Common)

This is the standard SIP that most investors use.

You invest a fixed amount every month into a mutual fund.

Example:

₹5,000 every month

₹10,000 every month

The amount remains the same unless you manually change it.

This type is best for:

- Salaried professionals

- Beginners

- Long-term investors

If you’re starting for the first time, regular SIP is the simplest and safest option.

2. Step-Up SIP (Best for Salaried Investors)

Step-up SIP allows you to increase your investment amount every year.

For example:

You start with ₹5,000 per month

Next year increase to ₹6,000

Then ₹7,000 and so on

As your salary grows, your investment grows too.

This is one of the smartest ways to build wealth because:

- You invest more without feeling burden

- Your savings rate improves

- Compounding accelerates

Most wealth builders use step-up SIP without realizing it.

3. Flexible SIP

Flexible SIP allows you to change the investment amount anytime.

You can:

- Increase amount

- Decrease amount

- Skip temporarily

This is useful for:

- Freelancers

- Business owners

- People with irregular income

However, beginners with stable salaries should prefer regular SIP for discipline.

4. Trigger SIP (Advanced)

Trigger SIP invests based on specific market conditions.

Example:

Invest when market falls 5%

Invest when NAV hits certain level

This requires market understanding and is usually not recommended for beginners.

For most investors, simple regular SIP works better.

Which SIP Type Should You Choose?

For most beginners in India:

Start with regular SIP.

Gradually move to step-up SIP as income increases.

Keep things simple.

Complicated strategies are not required to build wealth.

Consistency matters more than complexity.

Expected Returns From SIP (Realistic Numbers)

One of the most common questions beginners ask is:

How much return can I get from SIP?

Let’s be clear and realistic.

SIP does not guarantee fixed returns like a fixed deposit.

Returns depend on the type of mutual fund and market performance.

However, historically, equity mutual funds in India have delivered strong long-term returns.

Average SIP Returns in India

Here is a realistic expectation:

| Investment Type | Expected Long-Term Return |

|---|---|

| Equity Mutual Funds | 10–12% annually |

| Index Funds | 10–12% annually |

| Hybrid Funds | 8–10% annually |

| Debt Funds | 6–8% annually |

These are long-term averages (10+ years), not yearly guarantees.

Markets may go up or down in the short term,

but long-term investing smooths volatility.

Example: How SIP Builds Wealth Over Time

Let’s look at simple projections (assuming ~12% annual return).

₹3,000 Monthly SIP

| Time | Approx Value |

|---|---|

| 5 years | ₹2.4–2.7 lakh |

| 10 years | ₹7 lakh |

| 20 years | ₹30 lakh |

₹5,000 Monthly SIP

| Time | Approx Value |

|---|---|

| 10 years | ₹11–12 lakh |

| 20 years | ₹50 lakh+ |

| 25 years | ₹95 lakh – ₹1 crore |

₹10,000 Monthly SIP

| Time | Approx Value |

|---|---|

| 20 years | ₹1 crore+ |

| 25 years | ₹2 crore+ |

This is the power of long-term compounding.

Why Long-Term Matters More Than Returns

Many beginners focus too much on:

“Which fund gives highest return?”

But duration matters more.

Even an average 11–12% return over 20 years can build significant wealth.

Trying to chase highest-return funds often leads to poor decisions and frequent switching.

Consistency beats perfection.

Can SIP Make You Rich?

SIP alone won’t make you rich overnight.

But disciplined investing over 15–25 years can build substantial wealth.

Most middle-class crore-pati investors in India didn’t achieve it through trading.

They achieved it through:

- Regular investing

- Increasing SIP over time

- Staying invested long term

That’s the real SIP success formula.

Important: SIP Returns Are Not Linear

Markets don’t move in a straight line.

Some years:

+20% returns

Some years:

-10% or flat

This is normal.

SIP works best when you continue investing during market ups and downs.

Stopping SIP during market fall is one of the biggest mistakes beginners make.

Use a SIP Calculator for Accurate Planning

Instead of guessing returns, you can calculate future value using a SIP calculator.

This helps you:

- Set realistic goals

- Decide monthly investment

- Understand long-term growth

👉 Use our SIP Calculator here

SIP vs Lump Sum – Which is Better for Beginners?

Many new investors get confused between SIP and lump sum investing.

Both methods are useful, but they work differently.

Let’s understand which one is better for beginners.

What is Lump Sum Investment?

Lump sum means investing a large amount of money at once.

Example:

Investing ₹1 lakh or ₹5 lakhs in a mutual fund in one go.

Instead of investing monthly, you invest everything at once.

SIP vs Lump Sum: Key Differences

| Feature | SIP | Lump Sum |

|---|---|---|

| Investment style | Monthly fixed investment | One-time large investment |

| Best for | Salaried beginners | Investors with idle cash |

| Market timing risk | Low | High |

| Discipline | Very high | Depends on investor |

| Volatility impact | Averaged out | Directly affected |

| Stress level | Low | Higher |

When SIP is Better

SIP is better if:

- You earn monthly salary

- You are a beginner

- You don’t want to time the market

- You want disciplined investing

- You are investing for long-term goals

SIP reduces emotional stress and timing risk.

This is why most salaried investors prefer SIP.

When Lump Sum is Better

Lump sum investing can work better if:

- You have large idle money

- Markets are down or undervalued

- You have long-term horizon

- You understand market cycles

However, beginners often find it difficult to time the market correctly.

Which Should Beginners Choose?

For most beginners in India:

SIP is the safer and smarter option.

You don’t need to worry about market ups and downs.

You don’t need large capital.

You invest consistently and build wealth gradually.

If you receive a bonus or lump sum money, you can still invest it gradually through SIP or STP (Systematic Transfer Plan).

Best Strategy for Salaried Investors

Many experienced investors follow a simple approach:

Monthly income → SIP

Bonus/extra money → Lump sum or STP

This creates a balanced investment strategy.

Final Verdict: SIP or Lump Sum?

If you are just starting your investment journey:

Start with SIP.

It builds discipline, reduces timing risk and works well for long-term wealth creation.

Once your investment knowledge and capital grow, you can use both methods together.

If you haven’t yet started investing, read the complete beginner guide here:

👉 Start investing in India

SIP vs FD – Which is Better for Wealth Creation?

Many Indians compare SIP with Fixed Deposit (FD).

FD feels safe.

SIP feels risky.

But are they really comparable?

Let’s understand the difference clearly.

What is a Fixed Deposit (FD)?

A Fixed Deposit is a bank product where:

- You deposit money for a fixed period

- You earn fixed interest

- Returns are guaranteed

Typical FD returns in India range between 6–8% per year (depending on tenure and bank).

FDs are safe but offer limited growth.

SIP vs FD: Key Comparison

Feature | SIP (Equity Mutual Fund) | Fixed Deposit

Returns | 10–12% (long-term avg) | 6–8% fixed

Risk | Market-linked | Very low

Inflation beating | Yes (long-term) | Often no

Liquidity | High (after lock-in if any) | Moderate

Taxation | Capital gains tax | Interest fully taxable

Best for | Wealth creation | Capital protection

Which One Beats Inflation?

Inflation in India averages around 5–6% long term.

If your FD gives 6% and inflation is 6%:

Your real return is close to zero.

If SIP gives 11–12% long term:

After inflation, your real return is still positive.

That’s why SIP is generally better for long-term wealth creation.

Is SIP Riskier Than FD?

Yes, SIP invested in equity mutual funds is market-linked.

In short term, values fluctuate.

But over long periods (10–20 years), equity mutual funds have historically outperformed FDs significantly.

FD protects capital.

SIP grows capital.

Both have different roles.

When Should You Choose FD?

FD is better if:

- You need money in 1–3 years

- You are building emergency fund

- You want guaranteed returns

- You cannot tolerate market fluctuations

FD is stability.

When Should You Choose SIP?

SIP is better if:

- Your goal is 5+ years away

- You want wealth creation

- You want to beat inflation

- You are comfortable with short-term ups and downs

SIP is growth.

Smart Strategy: Use Both

Most smart investors don’t choose one over the other.

They use:

FD or liquid funds → Emergency fund

SIP in equity funds → Long-term wealth

This balance gives safety + growth.

Final Verdict: SIP or FD?

For short-term safety → FD

For long-term wealth → SIP

If you are under 40 and investing for retirement or financial freedom, SIP in equity mutual funds is generally more powerful.

But remember:

Invest according to your risk tolerance and goals.

Who Should Invest in SIP?

SIP is one of the most flexible investment methods available in India.

But is it suitable for everyone?

Let’s understand who should and should not invest in SIP.

SIP is Best For Beginners

If you are new to investing, SIP is one of the safest ways to begin.

You don’t need deep stock market knowledge.

You don’t need large capital.

You don’t need to track markets daily.

You simply invest a fixed amount every month and stay consistent.

This makes SIP ideal for first-time investors.

SIP is Ideal for Salaried Professionals

Salaried individuals earn monthly income.

SIP matches this perfectly.

You can invest a fixed amount every month immediately after receiving your salary.

This builds a strong saving and investing habit.

Over time, this discipline creates significant wealth.

SIP is Perfect for Long-Term Goals

SIP works best when your investment horizon is long.

Examples of long-term goals:

Retirement planning

Financial independence

Child’s education

Wealth creation

Home down payment

If your goal is 5 years or more away, SIP can be a powerful strategy.

SIP is Suitable for Small Investors

Many people believe investing requires a large amount.

That’s not true.

You can start SIP with as little as ₹500 per month.

Even small amounts, invested consistently over years, can grow into a large corpus due to compounding.

Starting early matters more than starting big.

Who Should NOT Rely Only on SIP?

SIP is powerful, but it is not suitable for every situation.

Short-Term Goals (Less than 2–3 Years)

If you need money soon, equity mutual fund SIP may not be ideal.

Markets fluctuate in short term.

For short-term goals, safer options like:

- Fixed deposits

- Liquid funds

- Short-term debt funds

may be more suitable.

Emergency Fund

Emergency money should never be invested in equity SIP.

Keep emergency fund in:

- Savings account

- Liquid funds

- Short-term FD

Investing emergency money in SIP can force you to withdraw during market downturns.

People Expecting Quick Profits

If someone expects:

“Double money in 1–2 years”

SIP is not the right tool.

SIP is designed for slow and steady wealth creation, not quick profits.

Ideal SIP Investor Profile

You are a perfect SIP candidate if:

- You have regular monthly income

- You want long-term wealth creation

- You can stay invested for 5–10+ years

- You want a simple investment method

- You want to beat inflation

For such investors, SIP is one of the best financial tools available.

How to Start SIP in India (Step-by-Step Guide)

Starting a SIP today is simple and completely online.

You don’t need to visit a bank.

You don’t need physical paperwork.

You don’t need large capital.

Here’s the exact step-by-step process.

Step 1: Complete Your KYC

Before investing in mutual funds, you must complete KYC (Know Your Customer).

You will need:

- PAN card

- Aadhaar card

- Bank account

- Mobile number linked to Aadhaar

Most platforms complete KYC digitally using OTP and video verification.

Once KYC is approved, you can start investing immediately.

Step 2: Choose Where to Invest

You have two main options.

Option 1: Direct Mutual Fund Platforms

You can invest directly through:

- AMC (Asset Management Company) websites

- Direct mutual fund apps

This avoids distributor commission and slightly improves long-term returns.

Option 2: Demat Account Platforms

If you want flexibility to invest in:

- Stocks

- ETFs

- Mutual funds

You can open a demat account with brokers.

The process is fully online and takes 15–20 minutes.

For beginners starting with SIP, either option works.

Keep it simple.

Step 3: Select the Right Mutual Fund

If you are a beginner, start with simple and diversified options:

- Nifty 50 Index Fund

- Large-cap mutual fund

- Flexi-cap fund

Avoid complex or high-risk funds initially.

You don’t need 5–6 funds to begin.

Even one good diversified fund is enough.

Step 4: Decide Your SIP Amount

Choose an amount that:

- You can comfortably invest every month

- Does not affect your daily expenses

- Can be increased later

Start small if needed.

Consistency matters more than amount.

Step 5: Set Auto-Debit and Confirm

Select:

- SIP date (for example, 5th of every month)

- Bank mandate

Once activated, your SIP runs automatically.

You don’t need to manually invest each month.

That’s the beauty of SIP.

When Will Your SIP Start?

KYC approval: Usually same day or within 1–2 days

SIP activation: Within 3–5 working days

After that, your investment journey officially begins.

If you haven’t yet understood the full investing roadmap, read this guide:

👉 Start Investing in India

Common SIP Mistakes to Avoid

SIP is simple, but many beginners still make mistakes that reduce returns or create panic.

Avoiding these common errors can significantly improve your long-term results.

1. Stopping SIP During Market Crash

This is the biggest mistake beginners make.

When markets fall, many investors panic and stop SIP.

But market corrections are actually beneficial for SIP investors.

When markets fall:

You buy more units at lower prices.

When markets recover:

Those extra units generate strong returns.

Stopping SIP during downturns breaks the compounding cycle.

Continue SIP unless your financial situation changes.

2. Expecting Quick Returns

SIP is not a shortcut to quick money.

Many beginners expect:

High returns in 1–2 years

Immediate profits

No market fluctuations

That’s unrealistic.

SIP works best over long periods like:

10 years

15 years

20 years

Patience is essential for wealth creation.

3. Choosing Too Many Mutual Funds

Some beginners start:

5–6 SIPs

Multiple similar funds

Overlapping portfolios

This creates confusion and reduces meaningful growth.

For beginners:

1–3 well-chosen funds are enough.

Keep your portfolio simple and easy to track.

4. Not Increasing SIP Over Time

If your salary increases but SIP remains same for years,

you lose potential growth.

Increase SIP whenever income rises.

Even a 10% yearly increase can dramatically improve long-term wealth.

This is called a step-up SIP strategy.

5. Investing Without Clear Goals

Many people start SIP randomly without knowing why.

Define your goals:

Retirement

Financial independence

Child education

Wealth creation

Goal-based investing helps you stay consistent and disciplined.

6. Ignoring Asset Allocation

Putting all money into equity funds without balance can increase risk.

Maintain a mix of:

Equity (for growth)

Debt (for stability)

This keeps your portfolio balanced and reduces panic during market volatility.

The Smart SIP Investor Mindset

Successful SIP investors follow a simple approach:

Start early

Stay consistent

Increase investment over time

Ignore short-term noise

Think long term

Avoiding basic mistakes is often more important than finding the “best” mutual fund.

Frequently Asked Questions About SIP in India

What is the minimum amount to start SIP?

You can start SIP with as little as ₹500 per month.

Many mutual funds allow minimum SIP investments between ₹500 and ₹1,000.

The important thing is to start early and stay consistent.

Is SIP safe in India?

SIP as a method is safe and disciplined.

However, returns depend on the mutual fund you choose and market performance.

Equity mutual funds can fluctuate in the short term but have historically delivered strong long-term returns.

For long-term investors, SIP is considered one of the safest ways to participate in equity markets gradually.

Can I stop SIP anytime?

Yes.

You can pause or stop your SIP anytime without penalty.

Your invested money remains in the mutual fund and continues to grow or fluctuate based on market performance.

Can I withdraw money from SIP anytime?

Yes, most mutual funds allow redemption anytime.

However:

Equity funds may have exit load if withdrawn within a short period.

ELSS funds have a 3-year lock-in.

For best results, SIP should be continued for long-term goals.

How long should I continue SIP?

Ideally:

Minimum: 5 years

Better: 10 years

Best: 15–20+ years

Longer duration allows compounding to work effectively.

Can SIP make you rich?

SIP alone will not create overnight wealth.

But consistent investing over 15–25 years can build substantial wealth.

Many long-term investors in India have built crore-level portfolios through disciplined SIP investing.

Final Thoughts: Should You Start SIP Today?

If you are serious about building long-term wealth, SIP is one of the simplest and most effective strategies available in India.

You don’t need market expertise.

You don’t need huge capital.

You just need consistency and patience.

Start small.

Stay disciplined.

Increase over time.

That’s how real wealth is created.

If you are completely new to investing, read this complete beginner guide first:

👉 How to Start Investing in India

The best time to start investing was yesterday.

The next best time is today.

7 thoughts on “What is SIP Investment? How It Builds Wealth in India (Beginner Guide 2026)”