If you want to invest ₹50,000 per month in India, the best strategy is to allocate most of the amount to equity mutual funds through SIP for long-term wealth creation, while keeping a small portion in debt or gold for stability.

A disciplined ₹50,000 monthly investment plan can build a multi-crore corpus over time through compounding.

If you can invest ₹50,000 per month, you have entered the serious wealth-building phase of your financial life.

At this stage, investing is no longer about small savings or experimentation. It is about building real long-term assets that can shape your financial future.

Many salaried professionals reach this level after years of working, promotions, and stable income growth. Expenses are under control, emergency funds are built, and now a significant amount is available every month for investing.

This is where true financial transformation begins.

Because if ₹50,000 per month is invested properly and consistently, it has the potential to create a multi-crore portfolio over time. Not through risky bets or shortcuts, but through disciplined investing and compounding.

But the biggest challenge is not lack of options.

The challenge is confusion.

Mutual funds, stocks, gold, PPF, NPS, different apps, different advice from different people. Everyone suggests something different, and most of it feels either too complex or too generic.

You don’t need complexity.

You need a clear system.

A system that tells you exactly where your ₹50,000 should go every month and why.

In this detailed guide, you will learn:

- How to invest ₹50,000 per month step by step

- Best SIP for 50000 per month strategy

- Expected returns over time

- Smart portfolio allocation

- How to scale this to financial freedom

- Mistakes to avoid

Let’s first understand what investing ₹50,000 per month can actually create over the long term.

What Can ₹50,000 Per Month Grow Into Over Time?

If you want to invest ₹50,000 per month in India, the best strategy is to allocate most of the amount to equity mutual funds through SIP for long-A ₹50,000 monthly investment is not just saving.

It is serious wealth creation in motion.

At this level, you are building assets that can shape your retirement, financial independence, and long-term security.

Most people underestimate how powerful consistent investing can be. They focus only on the monthly amount and ignore the impact of time and compounding.

If ₹50,000 per month is invested in good equity mutual funds through SIP and earns an average long-term return of around 12 percent annually, the potential wealth creation can be significant.

Estimated Returns for ₹50,000 Monthly Investment

| Investment Duration | Monthly Investment | Total Invested | Estimated Value |

|---|---|---|---|

| 5 Years | ₹50,000 | ₹30 Lakhs | ₹42–45 Lakhs |

| 10 Years | ₹50,000 | ₹60 Lakhs | ₹1.2 – ₹1.4 Crore |

| 15 Years | ₹50,000 | ₹90 Lakhs | ₹2.8 – ₹3.2 Crore |

| 20 Years | ₹50,000 | ₹1.2 Crore | ₹5 – ₹6.5 Crore |

These are not guaranteed returns. Markets will move up and down. But historically, disciplined equity investing over long periods has delivered around 11–13 percent annual returns.

This is why a ₹50,000 monthly SIP is considered a powerful wealth-building strategy for salaried professionals and long-term investors.

Why ₹50,000 Per Month Is a Wealth Creation Sweet Spot

At this investment level, you can:

- Build multi-crore retirement corpus

- Achieve financial independence faster

- Create long-term financial security

- Reduce dependence on active income

- Build generational wealth

Most people try to invest large lump sums occasionally.

But consistent monthly investing often builds more reliable wealth.

The real power is not in finding the highest return.

The real power is in staying invested long enough for compounding to work.

Before deciding exactly where to invest ₹50,000 every month, make sure your financial base is strong and stable.

Before You Invest ₹50,000 Per Month – Build a Strong Foundation

If you are able to invest ₹50,000 per month, you are already ahead of most investors.

But before you invest aggressively, your financial base must be strong.

Wealth building works best when your finances are stable and protected.

Many investors focus only on returns.

Smart investors focus on stability first.

Before starting a ₹50,000 monthly investment plan, make sure these three basics are in place.

1. Emergency Fund – Your Financial Safety Net

You should have at least 6 months of monthly expenses saved separately before investing aggressively.

This money should be kept in:

- Savings account

- Liquid mutual fund

- Sweep FD

Do not invest your emergency fund in equity.

This fund protects you during:

- Job loss

- Medical emergencies

- Unexpected expenses

- Income gaps

Without an emergency fund, you may be forced to stop SIPs or withdraw investments during bad times. That breaks compounding and delays wealth creation.

If your monthly expenses are ₹60,000, aim for at least ₹3–4 lakhs as an emergency fund.

2. Health Insurance and Term Insurance

Before building wealth, protect your income.

One major medical emergency can wipe out years of investments if you are not insured.

Basic protection checklist:

- Health insurance (₹10–20 lakh cover)

- Term insurance if you have dependents

Insurance is not an investment.

It is financial protection.

Once protection is in place, you can invest confidently for long-term growth.

3. Clear High-Interest Debt First

If you have:

- Credit card dues

- Personal loans

- High-interest EMIs

Clear them before investing aggressively.

Why?

Because paying 24–36 percent interest on debt while earning 12 percent from investments makes no sense financially.

Debt freedom improves cash flow and gives peace of mind.

Once Your Base Is Strong

When you have:

- Emergency fund

- Insurance

- No high-interest debt

You are ready to invest ₹50,000 per month properly.

Now comes the most important part.

How to Invest ₹50,000 Per Month – Smart Allocation Strategy

When you start investing ₹50,000 per month, the goal is not just to invest.

The goal is to build a structured portfolio that grows consistently and compounds into serious wealth over time.

Many investors make one mistake at this stage.

They either invest everything in one place or over-diversify into too many funds and products.

You don’t need complexity.

You need clarity and balance.

A simple, disciplined allocation works best for long-term wealth creation.

Ideal ₹50,000 Monthly Investment Allocation

Here is a practical and balanced allocation that works well for most salaried professionals and long-term investors.

| Investment Type | Monthly Amount | Purpose |

|---|---|---|

| Equity Mutual Funds (Core Growth) | ₹30,000 | Long-term wealth creation |

| Index / Flexi Cap Funds | ₹10,000 | Diversification and stability |

| Mid/Small Cap Exposure | ₹5,000 | Higher growth potential |

| Gold / Gold ETF | ₹3,000 | Inflation hedge and stability |

| Liquid / Debt Fund | ₹2,000 | Liquidity and flexibility |

This structure keeps the majority of money in equity for long-term growth while maintaining stability through diversification.

Why Equity Should Be the Core

If your goal is wealth creation and financial independence, equity mutual funds should form the core of your portfolio.

They offer:

- Long-term growth potential

- Compounding benefits

- Diversification across companies

- Professional management

- SIP discipline

A simple mutual fund structure is enough:

- One Nifty 50 index fund

- One flexi-cap fund

- One mid-cap fund

You do not need 7–8 funds.

You do not need frequent switching.

Simple portfolios often outperform complicated ones because they are easier to maintain consistently.

If you are new to mutual funds or SIP investing, you can also read our detailed guide on how SIP works in India and builds long-term wealth.

The goal here is not complexity.

The goal is consistency for the next 15–20 years.

In the next section, we will look at something even more powerful.

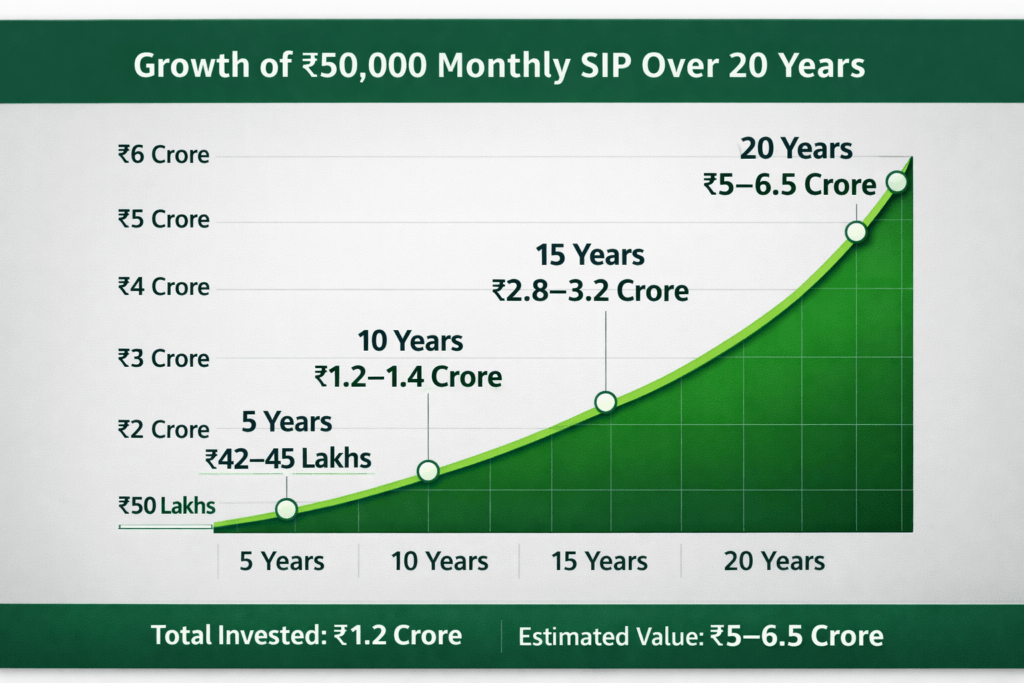

How Much Wealth Can ₹50,000 Per Month Create in 20 Years?

This is the question most serious investors want answered.

Not just where to invest, but what kind of future a ₹50,000 monthly investment can realistically create.

If ₹50,000 per month is invested consistently in equity mutual funds and earns an average long-term return of around 12 percent annually, the long-term results can be transformational.

Let’s look at this step by step.

After 5 Years

This is the early stage where discipline is built.

Compounding has started, but growth will look moderate.

- Total invested: ₹30 lakhs

- Estimated value: ₹42–45 lakhs

This phase builds investing habit and stability.

After 10 Years

Now compounding becomes clearly visible.

Your investments begin growing faster than your contributions.

- Total invested: ₹60 lakhs

- Estimated value: ₹1.2 to ₹1.4 crore

At this stage, many investors start seeing real wealth formation.

After 15 Years

This is where serious wealth creation begins.

Time and consistency multiply your money significantly.

- Total invested: ₹90 lakhs

- Estimated value: ₹2.8 to ₹3.2 crores

You are now entering financial freedom territory.

After 20 Years

Long-term disciplined investors are rewarded the most.

- Total invested: ₹1.2 crore

- Estimated value: ₹5 to ₹6.5 crores

You invested gradually every month.

But compounding did the heavy lifting.

Why Time Matters More Than Amount

Many people delay investing because they think ₹50,000 is not enough.

They wait for a higher salary.

They wait for a better time.

But in investing, starting early matters more than starting big.

Someone who starts investing ₹50,000 today and increases gradually will usually build more wealth than someone who waits 10 years and starts with a larger amount.

Time multiplies money.

Consistency multiplies time.

Now let’s look at the biggest reason why many investors fail even after investing good amounts.

Biggest Mistakes to Avoid While Investing ₹50,000 Per Month

Investing ₹50,000 per month gives you a powerful opportunity to build long-term wealth.

But even with a strong investment amount, certain mistakes can quietly reduce your returns.

Most investors do not fail because of bad funds.

They fail because of inconsistent behavior.

Avoiding these mistakes is often more important than finding the perfect investment.

1. Starting and Stopping SIP Frequently

Many investors begin with enthusiasm but stop investing when markets fall or expenses increase.

Reasons often include:

- Market volatility

- Temporary financial pressure

- Fear of losses

- Lack of long-term clarity

Stopping SIP breaks compounding.

Wealth is built through consistency, not intensity.

Even during market corrections, try to continue your investments if your financial situation allows.

Market falls are temporary.

Compounding rewards patience.

2. Overcomplicating the Portfolio

Some investors start adding too many funds and products:

- Multiple mutual funds

- Stocks without research

- Insurance-linked investments

- Random trending options

This creates confusion and reduces clarity.

You do not need a complicated portfolio to build wealth.

You need a disciplined and simple structure.

Too many investments make tracking difficult and often reduce long-term performance.

3. Trying to Time the Market

Waiting for the perfect time to invest is one of the biggest wealth destroyers.

Many people think:

- Market is high, I will invest later

- Market may fall more

- I will wait for correction

This delay prevents long-term compounding.

SIP works because it removes timing pressure.

You invest regularly and let markets average out over time.

Time in the market is more powerful than timing the market.

4. Not Increasing Investments with Income

This is the biggest silent mistake.

Income increases.

Lifestyle increases.

But investments remain the same.

If you continue investing ₹50,000 for many years despite salary growth, you slow down wealth creation.

Whenever your income increases, increase your SIP gradually.

Even a 10 percent yearly increase can dramatically boost long-term results.

5. Panic During Market Corrections

Markets will fall sometimes.

There will be corrections of:

- 10 percent

- 20 percent

- Sometimes more

This is normal.

If your investment horizon is long, these temporary declines should not change your strategy. Panic selling during such periods permanently damages compounding.

Calm investors build wealth.

Emotional investors interrupt it.

Avoid these mistakes and your ₹50,000 monthly investment can become a powerful long-term wealth engine.

Now let’s look at how to take this even further.

How to Turn ₹50,000 Per Month Into ₹1.5 Lakh Monthly Investing Over Time

₹50,000 per month is already a strong investment habit.

But if your goal is true financial independence and multi-crore wealth, this amount should grow as your income grows.

Most people increase their lifestyle with every salary hike.

Very few increase their investments.

That single difference decides who builds serious wealth.

Step 1 – Increase SIP with Every Salary Growth

Whenever your salary increases, increase your monthly investment by at least 10 to 20 percent.

Even a small increase of ₹5,000 to ₹10,000 per year can dramatically improve long-term wealth.

Example progression:

- Year 1 – ₹50,000 per month

- Year 2 – ₹60,000 per month

- Year 3 – ₹75,000 per month

- Year 5 – ₹1,00,000 per month

- Year 8 – ₹1.25 lakh per month

- Year 10 – ₹1.5 lakh per month

This gradual increase feels manageable and does not create sudden financial pressure.

What Difference Does This Make?

Let’s keep it practical.

If you invest ₹50,000 per month for 20 years at around 12 percent average return, you may build around ₹5–6 crores.

But if you increase your SIP by just 10 percent every year, your final corpus can grow dramatically and may cross ₹8–10 crores depending on consistency.

The difference is not luck.

The difference is discipline.

When Should You Increase Aggressively?

Increase investments strongly during:

- Job change with higher salary

- Promotion or bonus

- Loan closure

- Business income increase

- When expenses stabilize

Most people upgrade lifestyle first and investments later.

Wealth builders do the opposite.

They increase investments first.

Lifestyle adjusts automatically.

The Real Wealth Formula

Start with ₹50,000.

Stay consistent.

Increase gradually every year.

Stay invested long term.

You do not need complex strategies or daily tracking.

Consistency plus time plus gradual increase builds real financial freedom.

Final Thoughts – Is ₹50,000 Per Month Enough to Build Serious Wealth?

Yes. Investing ₹50,000 per month is more than enough to build serious long-term wealth.

Not because the amount is extremely high.

But because the discipline and consistency behind it are powerful.

If invested properly with a clear structure, ₹50,000 per month can help you:

- Build a multi-crore retirement corpus

- Achieve financial independence earlier

- Create long-term financial security

- Reduce dependence on active income

- Build generational wealth

You do not need perfect market timing.

You do not need risky shortcuts.

You do not need complicated strategies.

You need a system you can follow calmly for years.

Start with ₹50,000.

Stay consistent.

Increase when income grows.

Give your investments time to compound.

Over time, this simple habit can quietly transform your financial future.

Not overnight.

But steadily.

And steady wealth is the kind that lasts.

What to Read Next

Continue your investment journey with these guides:

- How to Invest ₹10,000 Per Month in India

- How to Invest ₹20,000 Per Month in India

- How to Invest ₹30,000 Per Month in India

- Best Investment Options in India for Beginners

- What is SIP and How It Works in India

Build knowledge slowly.

Invest consistently.

Let time do the heavy lifting.

That is the Finari way.

1 thought on “How to Invest ₹50,000 Per Month in India (2026 Guide)”