If you want to invest ₹20,000 per month in India, the best strategy is to allocate most of the amount to equity mutual funds through SIP, keep a small portion in debt or liquid funds for stability, and increase investments gradually as income grows. A disciplined ₹20,000 monthly investment plan can build significant long-term wealth through compounding.

If you can invest ₹20,000 per month, you are no longer just saving money. You are actively building assets.

This is the stage where salaried professionals move from basic financial planning to serious wealth creation.

Many people search:

- Where to invest ₹20,000 per month?

- What is the best SIP for 20000 per month?

- How much are invest 20000 monthly returns?

- Can ₹20,000 per month create ₹1 crore?

The good news is yes – if structured properly.

But the key is not chasing high returns.

The key is building a balanced, sustainable 20000 monthly investment plan that you can follow for years.

In this detailed guide, you will learn:

- How to invest ₹20,000 per month step-by-step

- Best SIP for ₹20,000 per month strategy

- Expected returns over 5, 10, 15 and 20 years

- Allocation based on risk profile

- How to scale beyond ₹20k

- Common mistakes to avoid

Let’s first understand what investing ₹20,000 per month can actually achieve over time.

What Can ₹20,000 Per Month Grow Into Over Time?

A ₹20,000 monthly investment may not feel extraordinary in the beginning, but over time it can create serious wealth.

Most people focus only on how much they invest.

Experienced investors focus on how long they stay invested.

Consistency and time are what turn a ₹20,000 monthly SIP into a powerful long-term asset.

If you invest ₹20,000 per month in good equity mutual funds and earn an average long-term return of around 12 percent annually, the numbers can become meaningful over time.

Here is a realistic view of potential growth.

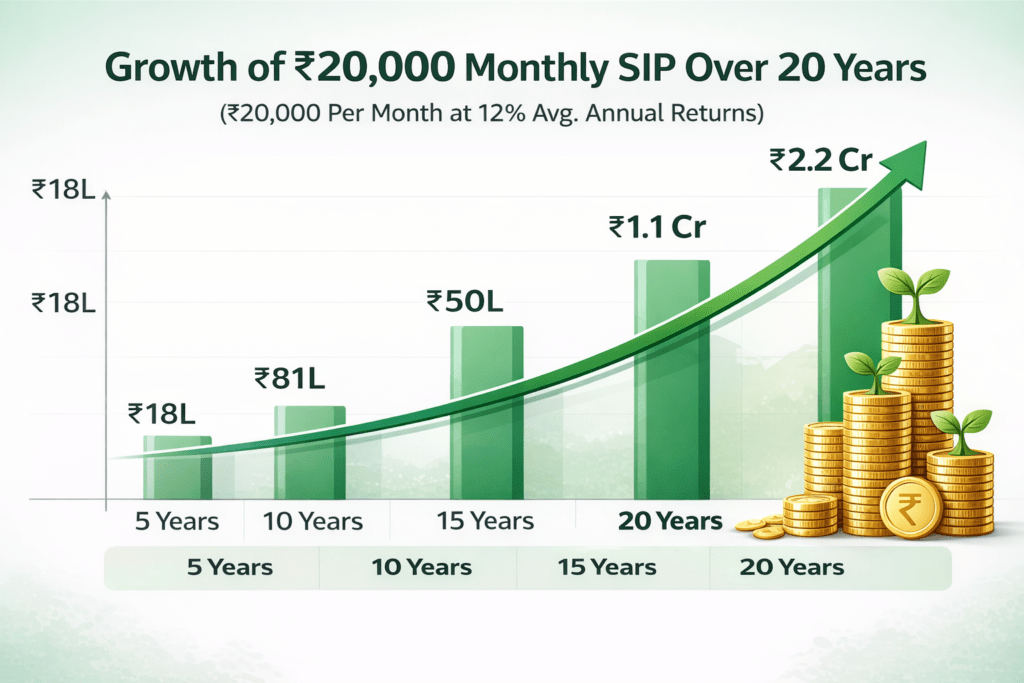

Estimated Returns for ₹20,000 Monthly Investment

| Investment Duration | Monthly Investment | Total Invested | Estimated Value |

|---|---|---|---|

| 5 Years | ₹20,000 | ₹12 Lakhs | ₹16–18 Lakhs |

| 10 Years | ₹20,000 | ₹24 Lakhs | ₹45–50 Lakhs |

| 15 Years | ₹20,000 | ₹36 Lakhs | ₹95 Lakhs – ₹1.1 Cr |

| 20 Years | ₹20,000 | ₹48 Lakhs | ₹1.8 – ₹2.2 Crore |

These are not guaranteed returns. Markets will fluctuate. Some years will deliver lower returns, and some years will be strong.

But historically, long-term SIP investing in equity mutual funds has delivered around 11–13 percent annualized returns over long periods.

This is why many financial planners suggest SIP for ₹20,000 per month as a strong long-term wealth strategy for salaried professionals.

Why This Amount Is Powerful

If invested consistently, ₹20,000 per month can:

- Build a retirement corpus

- Create wealth for buying a house

- Fund children’s education

- Provide financial independence

- Reduce dependency on salary in future

Many people underestimate what consistent investing can do over 15–20 years.

They overestimate what can happen in one year and underestimate what can happen in twenty.

If you are disciplined and patient, this ₹20,000 monthly investment plan can become one of the strongest financial decisions of your life.

But before deciding where to invest ₹20,000 every month, you must first build a strong financial base.

Before You Invest ₹20,000 Per Month – Strengthen Your Foundation

If you are investing ₹20,000 per month, you are entering serious wealth-building territory.

But before allocating this amount to SIPs or mutual funds, make sure your financial foundation is strong.

Many salaried professionals start investing aggressively without stabilizing their basics. Then when an emergency happens, they withdraw investments or stop SIPs completely. This breaks compounding and slows wealth creation.

Before investing ₹20,000 monthly, ensure these three pillars are in place.

1. Emergency Fund – At Least 6 Months of Expenses

Since your investment amount is higher, your responsibilities may also be higher.

Keep at least 6 months of essential expenses in a savings account or liquid fund.

For example:

If your monthly expenses are ₹40,000

Your emergency fund should be ₹2.5 to ₹3 lakhs

This protects your SIP from disruption during:

- Job loss

- Medical emergency

- Unexpected family expenses

An emergency fund is not an investment.

It is financial protection.

2. Adequate Health Insurance

If you are investing ₹20,000 monthly but do not have personal health insurance, you are taking unnecessary risk.

Corporate insurance is good, but not enough.

A sudden medical expense can wipe out years of investments. Proper health insurance ensures your wealth-building journey continues uninterrupted.

3. No High-Interest Debt

Before investing ₹20,000 monthly, clear:

- Credit card dues

- Personal loans with high interest

- Consumer EMIs

If you are paying 30 percent interest on a credit card and earning 12 percent from mutual funds, you are moving backward financially.

Clear high-interest debt first.

Then invest aggressively.

Why This Step Is Critical

When your foundation is strong:

- You do not panic during market volatility

- You stay invested long term

- You avoid premature withdrawals

- You allow compounding to work properly

Once these basics are in place, you can confidently build a structured ₹20,000 monthly investment plan.

Now let’s move to the most important part:

Where exactly should this ₹20,000 go?

How to Invest ₹20,000 Per Month in India (Simple Allocation Strategy)

When your monthly investment amount reaches ₹20,000, your focus should shift from random investing to structured wealth building.

At this level, you don’t need complicated strategies or risky bets.

You need a clear system that balances growth, safety, and flexibility.

Most beginners make one mistake here.

They try to find the “best investment” instead of building the best allocation.

But long-term wealth is not built by one perfect fund.

It is built by a consistent monthly structure.

If you are still new to investing, you can first read our complete beginner roadmap on

Best Investment Options in India for Beginners, where we explain all major investment choices step by step.

Now let’s build a simple ₹20,000 monthly investment plan.

Recommended ₹20,000 Monthly Investment Allocation

For most salaried professionals and beginners, this structure works extremely well.

| Investment Type | Monthly Amount | Purpose |

|---|---|---|

| Equity Mutual Funds | ₹12,000 | Long-term wealth creation |

| Index or Flexi Cap Fund | ₹4,000 | Stability and diversification |

| Gold ETF or Gold Fund | ₹2,000 | Hedge and safety |

| Liquid Fund / Savings | ₹2,000 | Emergency flexibility |

This 20000 monthly investment plan gives:

- Strong long-term growth

- Diversification across assets

- Stability during market volatility

- Liquidity when needed

It also ensures you are not putting all money into a single category.

Why Mutual Funds Should Be Your Core Investment

If you are investing ₹20,000 monthly, mutual funds should form the backbone of your portfolio.

They provide:

- Diversification across multiple companies

- Professional fund management

- Easy SIP automation

- Long-term compounding

You don’t need 7–8 funds.

You don’t need daily tracking.

A simple structure is enough:

- One index fund (Nifty 50)

- One flexi cap fund

- Optional mid-cap exposure later

If you are completely new to SIP investing, read our detailed beginner guide on

What is SIP and How It Works in India to understand the basics.

Where to Invest ₹20,000 Per Month for Best Results

If your goal is long-term wealth creation, equity mutual funds should get the highest allocation.

If your goal is safety and stability, increase debt or liquid portion slightly.

But for most working professionals in their 20s, 30s, and early 40s:

Higher equity allocation = better long-term results.

You can also check our detailed guide on

How Much Money Do You Need to Start Investing in India

if you are still building your monthly investment habit.

What Type of Investor Are You?

Before deciding the exact allocation of your ₹20,000 monthly investment, one important question needs to be answered.

What type of investor are you?

Not everyone should invest ₹20,000 the same way.

Your investment structure should match your comfort with risk, time horizon, and financial goals.

Many people copy random portfolios from the internet or friends.

But the best investment plan is the one you can follow calmly for years.

Let’s keep this simple.

Conservative Investor – Stability First

If you feel uncomfortable when markets fall or prefer steady and predictable growth, you fall into the conservative category.

You want growth, but you also want stability.

For you, protecting capital is as important as growing it.

A conservative ₹20,000 monthly investment plan can look like this:

| Allocation Type | Monthly Amount |

|---|---|

| Equity Mutual Funds | ₹10,000 |

| Hybrid/Debt Funds | ₹6,000 |

| Gold | ₹2,000 |

| Liquid Fund | ₹2,000 |

This structure reduces volatility.

Your portfolio will grow steadily without large ups and downs.

Returns may be slightly lower than aggressive portfolios, but your peace of mind will remain high.

And peace of mind keeps you invested.

Balanced Investor – Growth + Stability

Most salaried professionals fall into this category.

You are comfortable with market ups and downs but still want some safety built into your portfolio.

This is usually the best approach for long-term wealth creation.

A balanced ₹20,000 monthly investment plan:

| Allocation Type | Monthly Amount |

|---|---|

| Equity Mutual Funds | ₹14,000 |

| Index/Flexi Cap Fund | ₹4,000 |

| Gold or Debt | ₹2,000 |

This allocation focuses on long-term growth while still giving diversification and stability.

If your goal is wealth creation, home buying, or financial independence, this structure works very well.

Growth-Oriented Investor – Maximum Wealth Focus

If you are investing for 15–20 years and market volatility does not disturb you emotionally, you can adopt a growth-focused strategy.

This is ideal for:

- Young professionals

- High-income earners

- Long-term investors

- People with stable jobs

A growth-oriented allocation:

| Allocation Type | Monthly Amount |

|---|---|

| Equity Mutual Funds | ₹16,000 |

| Index Fund | ₹4,000 |

This maximizes compounding potential.

However, you must be mentally prepared for temporary market falls of 20–30 percent during corrections. If such falls make you panic, this allocation is not suitable.

There Is No Perfect Allocation

The best allocation is not the one with highest returns.

The best allocation is the one you can follow consistently for years without panic.

Because real wealth is built by consistency, not by chasing returns.

If you want a detailed beginner-friendly investment structure, you can also read our guide on

Best Mutual Funds for Beginners in India, where we explain how to choose funds step by step.

Now let’s move to the most exciting part.

How much wealth can ₹20,000 per month actually build over time?

Biggest Mistakes People Make While Investing ₹20,000 Per Month

Investing ₹20,000 per month can build serious long-term wealth.

But small mistakes can silently destroy returns.

Most investors don’t fail because markets are bad.

They fail because their behaviour becomes inconsistent.

If you avoid the mistakes below, your probability of building wealth increases dramatically.

1. Starting SIP and Stopping Frequently

Many people start SIPs with excitement but stop them after a few months.

Reasons include:

- Market falling

- Temporary expenses

- Fear of losses

- No clear plan

Stopping SIP repeatedly breaks compounding.

Wealth is not built by investing occasionally.

It is built by investing consistently.

Even during market corrections, continue your SIP if possible.

Market falls are temporary.

Compounding is permanent.

2. Investing Without Clear Allocation

Some investors put the entire ₹20,000 into one random fund or stock.

Others keep switching investments every few months.

This creates confusion and weak long-term results.

Instead, follow a simple structured allocation like we discussed earlier.

A clear 20000 monthly investment plan removes emotional decisions and keeps investing automatic.

3. Trying to Time the Market

Many beginners wait for the “perfect time” to invest.

They think:

Market is high – I will invest later

Market may fall – I will wait

News looks negative – let me pause

This waiting habit delays wealth creation.

SIP works because it removes timing pressure.

You invest every month.

Markets adjust over time.

Compounding continues.

Time in the market is more important than timing the market.

4. Not Increasing SIP When Salary Grows

This is the biggest silent mistake.

Salary increases.

Lifestyle increases.

But SIP remains the same.

If you keep investing ₹20,000 for 10 years without increasing it despite salary growth, you slow down your wealth creation.

Whenever your income increases, try to increase SIP by at least 10 percent.

This step alone can double your final corpus over long periods.

5. Panic During Market Falls

Markets will fall.

Sometimes 10 percent.

Sometimes 20 percent.

Sometimes even more.

This is normal.

If you are investing ₹20,000 monthly for long-term goals like retirement or wealth creation, short-term market fluctuations should not change your strategy.

Panic selling during market falls permanently damages compounding.

Calm investors build wealth.

Emotional investors interrupt it.

How to Turn ₹20,000 Per Month Into ₹50,000 Per Month Over Time

₹20,000 per month is not a small amount.

But it should not remain ₹20,000 forever.

The real power of wealth creation comes when your investments grow along with your income. Many salaried professionals increase their lifestyle every year but forget to increase their investments.

If you continue investing ₹20,000 per month for the next 20 years, you can still build strong wealth. But if you increase this amount gradually as your salary grows, the final corpus can become significantly larger.

This is called a step-up investment strategy.

Step 1 – Increase SIP With Every Salary Hike

Whenever your income increases, increase your SIP by at least 10 to 20 percent.

Even a small increase of ₹2,000 to ₹5,000 per year creates a huge difference over long periods.

For example:

Year 1 – ₹20,000 per month

Year 2 – ₹25,000 per month

Year 3 – ₹30,000 per month

Year 5 – ₹40,000 per month

Year 8 – ₹50,000 per month

Without feeling sudden pressure, your investments grow naturally with your income.

You can use our FREE SIP & Lump Sum Calculator to check returns

What Difference Does This Make?

Let’s keep this practical.

If you invest ₹20,000 per month for 20 years at around 12 percent average return, you may build around ₹2 crore.

But if you increase your SIP by just 10 percent every year, your final wealth can grow dramatically and potentially cross ₹3–4 crores over long periods depending on consistency.

The difference is not timing.

The difference is discipline.

When Should You Increase Investments Aggressively?

There are certain stages where you should strongly increase investments:

- After a job switch with higher salary

- After clearing a loan

- After major salary hikes

- After bonuses

- When expenses stabilize

Most people upgrade lifestyle first and investments later.

Wealth builders do the opposite.

They increase investments first.

Lifestyle adjusts automatically.

The Real Wealth Formula

Start with ₹20,000.

Stay consistent.

Increase every year.

Stay invested long term.

You don’t need complicated strategies or constant monitoring.

Consistency plus time plus gradual increase builds long-term financial freedom.

Final Thoughts – Is ₹20,000 Per Month Enough to Build Serious Wealth?

Yes. Investing ₹20,000 per month is more than enough to build serious long-term wealth.

Not because the amount is huge.

But because the habit is powerful.

If invested consistently with a clear structure, a ₹20,000 monthly investment plan can help you:

- Build a retirement corpus

- Create long-term financial security

- Achieve financial independence

- Reduce dependence on salary

- Handle future life goals comfortably

The biggest advantage you have is time and consistency.

You don’t need to predict markets.

You don’t need to chase trending investments.

You don’t need complicated strategies.

You just need a system you can follow every month without stress.

Start with ₹20,000.

Stay consistent.

Increase when income grows.

Give your investments time to compound.

Over the years, this simple discipline can quietly transform your financial future.

Not overnight.

But steadily.

And steady wealth is the kind that lasts.

What to Read Next

If you are building your monthly investment journey step by step, read these next:

If you are starting smaller:

How to Invest ₹5,000 Per Month in India

If you want a structured beginner roadmap:

Best Investment Options in India for Beginners

To understand SIP deeply:

What is SIP and How It Works in India

Build knowledge slowly.

Invest consistently.

Let time do the heavy lifting.

That is the Finari way.

1 thought on “How to Invest ₹20,000 Per Month in India (2026 Guide)”