Most people in India save money.

Very few know where to invest money in India for long term wealth creation.

Some choose Fixed Deposits because they feel safe.

Some buy random mutual funds based on friend recommendations.

Some invest in gold because “it always works.”

Others keep waiting for the “right time.”

The result? Slow wealth growth.

Long-term investing is not about chasing high returns.

It is about choosing the right assets, staying invested, and allowing compounding to work.

If you are earning regularly — whether ₹20,000 or ₹1,00,000 per month — this guide will help you understand:

- Where to invest for 5, 10, 15, 20+ years

- Which options are safe vs growth-focused

- How to plan for retirement properly

- What to do before starting long-term investing

- Sample portfolio allocations for different time horizons

This is not a generic list of investment options.

This is a structured roadmap.

Where to Invest Money in India for Long Term?

If you are investing for more than 5–10 years, the best long-term investment options in India are equity mutual funds (especially index and flexi-cap funds), Public Provident Fund (PPF), National Pension System (NPS), EPF for salaried individuals, and limited allocation to gold. The right mix depends on your time horizon, risk appetite, and financial goals.

| Time Horizon | Recommended Investment |

|---|---|

| 5 Years | Debt + Hybrid Funds |

| 10+ Years | Equity Mutual Funds + Gold |

| 20+ Years | Equity Heavy Portfolio |

| Retirement | Balanced Equity + Debt |

Before we discuss where to invest, there is one important rule:

Long-term investing should only begin after building financial protection.

Let’s start there.

Before You Start Long-Term Investing

Before deciding where to invest money in India for long term, you must build a financial base.

Long-term investments work only when you are not forced to withdraw them during emergencies.

Many people start SIPs and then stop within 1–2 years because of:

- Job loss

- Medical emergency

- Unexpected expenses

- Existing debt pressure

That breaks compounding.

So before investing for 10, 20 or 30 years, complete this checklist.

1. Build an Emergency Fund

An emergency fund should cover 6–12 months of essential expenses.

If your monthly expenses are ₹40,000, your emergency fund should be:

₹2.4 lakh to ₹4.8 lakh

Keep this money in:

- Savings account

- Liquid mutual fund

- Sweep FD

Do not invest this in equity.

This money is not for growth. It is for protection.

2. Take Health Insurance

One medical emergency can destroy years of savings.

Even if you have corporate insurance, take a personal health insurance policy.

Why?

If you change jobs, your coverage should continue.

Health costs in India are rising every year. Long-term investing only works when unexpected hospital bills do not disturb your portfolio.

3. Take Term Insurance (If You Have Dependents)

If someone depends on your income, term insurance is mandatory.

It is not an investment.

It is income protection.

Coverage should ideally be 15–20 times your annual income.

If you earn ₹10 lakh per year, coverage should be ₹1.5–2 crore.

4. Clear High-Interest Debt

If you are paying:

- 36% credit card interest

- 18% personal loan interest

No investment can consistently beat that.

Clear high-interest debt first.

Then invest.

Why This Step Matters

Long-term investing requires:

- Stability

- Discipline

- Consistency

Without financial protection, you will break your investments during market corrections.

And that destroys long-term wealth creation.

Now that your foundation is clear, let’s understand why long-term investing is powerful.

Benefits of Long-Term Investments

Long-term investing is not just about earning higher returns.

It changes how money behaves.

When you stay invested for 10, 20 or 30 years, three powerful forces start working in your favour — time, compounding and discipline.

Let’s understand each benefit clearly.

1. Power of Compounding

Compounding means earning returns on your returns.

In the early years, growth looks small.

But after 10–15 years, growth becomes exponential.

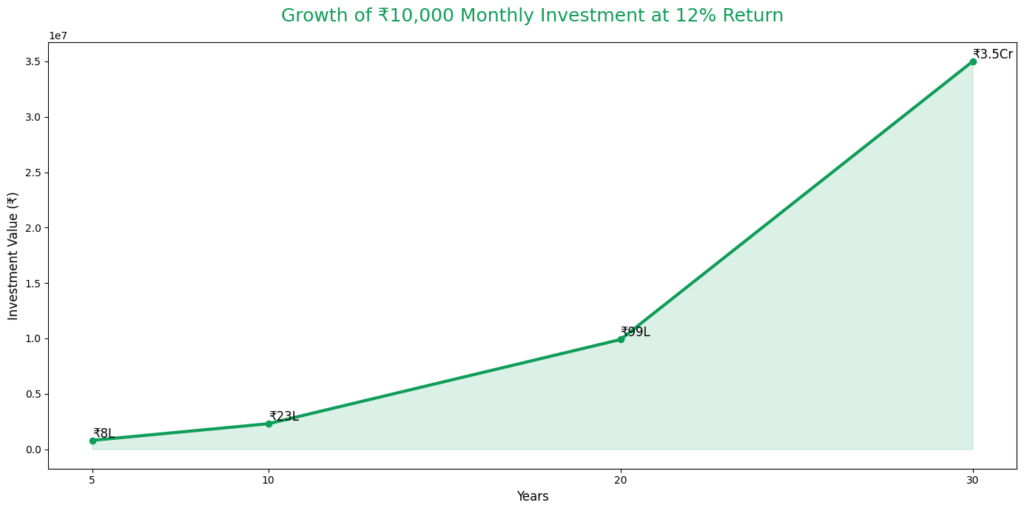

Here is a simple example:

If you invest ₹10,000 per month at 12% annual return:

| Years | Total Invested | Approx Value at 12% |

|---|---|---|

| 5 Years | ₹6,00,000 | ₹8,00,000+ |

| 10 Years | ₹12,00,000 | ₹23,00,000+ |

| 20 Years | ₹24,00,000 | ₹99,00,000+ |

| 30 Years | ₹36,00,000 | ₹3.5 Crore+ |

Notice something important.

Between 5 and 10 years, growth is decent.

Between 20 and 30 years, growth explodes.

That is compounding.

The longer you stay invested, the faster wealth grows.

2. Security from Short-Term Volatility

Markets fluctuate daily.

In the short term (1–3 years), returns can be unpredictable.

But historically, over longer periods, equity markets have rewarded patient investors.

Long-term investing reduces the impact of:

- Temporary market crashes

- Political events

- Global news

- Short-term fear

Time smooths volatility.

3. Lesser Effect of Market Fluctuations

If you invest for:

- 1 year → market timing matters

- 3 years → timing matters

- 15 years → consistency matters more than timing

Over longer horizons, temporary corrections look small on charts.

This is why equity mutual funds are recommended for 10+ years.

4. Goal-Centric Planning

Long-term investing helps you align money with life goals.

For example:

- Buying a house in 10 years

- Child’s education in 15 years

- Retirement in 25–30 years

Instead of random investing, you assign investments to goals.

This creates clarity and discipline.

5. Convenience

Long-term investing requires fewer decisions.

You do not need to track markets daily.

A simple monthly SIP into quality funds can work effectively over decades.

You invest.

You review once a year.

You continue.

Simple systems outperform complicated strategies.

6. Flexible Investment Options

In India, long-term investing offers multiple instruments:

- Equity mutual funds

- Index funds

- Public Provident Fund (PPF)

- National Pension System (NPS)

- Gold

- Real estate

- EPF

You can adjust asset allocation based on age and risk appetite.

7. More Time to Optimise Returns

Long investment horizons give you time to:

- Shift from aggressive to balanced portfolio

- Try different fund categories

- Rebalance allocations

- Correct mistakes

Short-term investing does not give this flexibility.

8. Who Should Consider Long-Term Investing?

Long-term investing is ideal for:

- Salaried professionals

- Business owners

- Young earners in their 20s and 30s

- Parents planning children’s future

- Anyone planning retirement

If your goal is more than 5 years away, long-term investing should be your strategy.

Now that you understand why long-term investing works, the next question becomes:

How much money do you actually need for retirement?

Because long-term investing without a target number is incomplete.

How to Calculate Your Retirement Corpus Properly

Long-term investing without a target number is incomplete.

If you do not know how much money you need for retirement, you cannot decide:

- How much to invest

- Where to invest

- How aggressively to invest

- How long you need to stay invested

So before choosing investment options, let’s calculate your retirement corpus properly.

Step 1: Estimate Your Current Monthly Expenses

Start with your present lifestyle cost.

Example:

If your current monthly expenses are ₹50,000, your annual expense is:

₹50,000 × 12 = ₹6,00,000 per year

Step 2: Adjust for Inflation

Inflation reduces purchasing power every year.

If inflation averages 6%, your expenses will double roughly every 12 years.

Let’s assume:

- Current age: 30

- Retirement age: 60

- Years to retirement: 30

- Current annual expense: ₹6,00,000

- Inflation: 6%

After 30 years, your annual expense will be approximately:

₹6,00,000 × (1.06)^30 ≈ ₹34,00,000 per year

That means you will need ₹34 lakh per year at retirement just to maintain today’s lifestyle.

Step 3: Estimate Retirement Duration

If you retire at 60 and live until 85, you need income for 25 years.

So total requirement is not just one year’s expense — it is 25 years of inflation-adjusted expense.

Step 4: Calculate Retirement Corpus

A simple rule used in financial planning:

Retirement Corpus ≈ 25 × Annual Expense at Retirement

So in our example:

₹34 lakh × 25 = ₹8.5 crore (approx.)

That is your target retirement corpus.

Retirement Corpus Example Table

| Parameter | Value |

|---|---|

| Current Monthly Expense | ₹50,000 |

| Years to Retirement | 30 Years |

| Inflation Assumed | 6% |

| Expense at Retirement | ₹34 Lakh / Year |

| Required Corpus | ₹8–9 Crore |

Important: This Is a Simplified Model

In reality, retirement planning also considers:

- Expected return during retirement

- Pension income

- EPF/NPS withdrawals

- Health inflation

- Partial asset allocation shift

But this gives you a strong starting framework.

Now the real question:

How should you invest based on different time horizons?

Because someone investing for 5 years should not invest the same way as someone investing for 30 years.

Where to Invest Based on Time Horizon

Not all long-term investments are the same.

Your strategy should change depending on how many years you have.

A person investing for 5 years should not take the same risk as someone investing for 30 years.

Let’s break it down clearly.

1. Investment Plan for 5 Years

Suitable For:

- Buying a car

- Higher education

- House down payment

- Short-to-medium term goals

Risk Capacity:

Low to Moderate

Equity can fluctuate heavily in 5 years. Capital protection matters more than aggressive growth.

Recommended Allocation

| Asset Class | Suggested Allocation |

|---|---|

| Debt Mutual Funds | 50% |

| Hybrid Funds | 30% |

| Gold | 10% |

| Large Cap Equity | 10% |

Focus: Stability first, growth second.

2. Investment Plan for 10 Years

Suitable For:

- Child’s education

- Home purchase

- Major life goals

Risk Capacity:

Moderate

Over 10 years, equity risk reduces significantly.

Suggested Allocation

| Asset Class | Suggested Allocation |

|---|---|

| Equity Mutual Funds | 50% |

| Hybrid Funds | 20% |

| Debt Funds | 20% |

| Gold | 10% |

Focus: Balanced growth.

3. Investment Plan for 15 Years

Now compounding starts becoming powerful.

Risk Capacity:

Moderate to High

Suggested Allocation

| Asset Class | Suggested Allocation |

|---|---|

| Equity Mutual Funds (Index + Flexi Cap) | 65% |

| Debt Funds | 20% |

| Gold | 10% |

| International Exposure | 5% |

Focus: Growth with risk management.

4. Investment Plan for 20 Years

Suitable For:

- Child’s higher education

- Early retirement goal

- Financial independence planning

- Long-term wealth creation

Risk Capacity:

High (if you can stay disciplined)

Over 20 years, equity volatility becomes significantly less dangerous. Time absorbs market corrections.

Suggested Allocation

| Asset Class | Suggested Allocation |

|---|---|

| Equity Mutual Funds (Index + Flexi Cap) | 70% |

| Mid & Small Cap Funds | 10% |

| Debt Funds | 15% |

| Gold / International Funds | 5% |

Focus: Aggressive growth with limited downside cushion.

5. Investment Plan for 25 Years

At 25 years, compounding becomes extremely powerful.

This duration is ideal for:

- Retirement (if starting at 30–35)

- FIRE planning

- Generational wealth building

Risk Capacity:

High (if emotionally disciplined)

Suggested Allocation

| Asset Class | Suggested Allocation |

|---|---|

| Equity Mutual Funds | 75% |

| Mid & Small Cap | 10% |

| Debt Funds | 10% |

| Gold / International | 5% |

Focus: Maximum compounding.

6. Investment Plan for 30 Years

This is pure wealth-building mode.

If you start at 25–30 years old, this is your retirement window.

Risk Capacity:

High

Suggested Allocation

| Asset Class | Suggested Allocation |

|---|---|

| Equity Mutual Funds (Index Heavy) | 80% |

| Mid & Small Cap | 10% |

| Debt Funds | 5% |

| Gold / International | 5% |

Focus: Long-term equity dominance.

7. Asset Allocation During Retirement

Once you retire, strategy changes.

Now the goal is:

- Capital protection

- Stable income

- Controlled withdrawals

Suggested Retirement Allocation

| Asset Class | Suggested Allocation |

|---|---|

| Debt Funds / Senior Citizen Schemes | 50% |

| Equity (Large Cap / Index) | 30% |

| Cash / Liquid Funds | 10% |

| Gold | 10% |

Best Long-Term Investment Options in India

There is no single “best” long-term investment.

The right option depends on:

- Time horizon

- Risk appetite

- Income stability

- Financial goals

Let’s understand the major long-term investment options in India and where they fit.

1. Equity Mutual Funds (Primary Wealth Builder)

For most people, equity mutual funds should be the foundation of long-term investing.

They invest in the stock market on your behalf and are professionally managed.

For long-term goals (10+ years), equity mutual funds historically deliver better returns than traditional savings products.

You can choose:

- Index Funds (tracking Nifty 50 or Sensex)

- Flexi Cap Funds

- Large & Mid Cap Funds

If you are just starting, read:

- What is SIP investment? How it builds wealth in India

- Best Investment Options for Beginners in India

SIP vs Lump Sum?

If you invest monthly, use SIP.

If you have surplus money, you can invest via lump sum – preferably in staggered manner.

You can check our SIP & Lumpsum calculator

2. Index Funds (Simple & Low-Cost)

Index funds track market indices like:

- Nifty 50

- Sensex

They do not try to “beat” the market.

They aim to match it.

Advantages:

- Low expense ratio

- Simple strategy

- Suitable for 15–30 year investing

For long-term investors who want simplicity, index investing is powerful.

3. Public Provident Fund (PPF) – Safe Long-Term Option

PPF is a government-backed scheme with 15-year lock-in.

Suitable for:

- Conservative investors

- Tax saving under 80C

- Portfolio stability

Returns are moderate, but safety is high.

It should complement equity — not replace it.

4. National Pension System (NPS)

NPS is designed for retirement planning.

It invests in a mix of equity and debt.

Advantages:

- Additional tax benefit under 80CCD(1B)

- Structured retirement approach

- Automatic asset allocation option

Good for retirement-focused long-term investing.

5. EPF (Employee Provident Fund)

If you are salaried, EPF is already part of your retirement planning.

Many people ignore its power.

Over 25–30 years, EPF contributions grow significantly due to compounding.

Do not withdraw EPF unnecessarily.

6.. Direct Stocks (For Advanced Investors)

Direct stock investing can generate high returns.

But it requires:

- Research

- Patience

- Emotional control

- Ability to tolerate volatility

For beginners, mutual funds are usually better.

If you are interested in building stock knowledge, start small.

7. Gold (Portfolio Diversifier)

Gold protects against:

- Inflation

- Currency risk

- Economic uncertainty

But gold alone does not build massive wealth.

It should ideally be 5–10% of your portfolio.

Sovereign Gold Bonds are more efficient than physical gold.

8. Real Estate

Real estate is a traditional wealth builder in India.

But consider:

- High capital requirement

- Low liquidity

- Maintenance cost

- City-dependent returns

For early-stage investors, equity mutual funds often provide better flexibility.

Why SIP in Equity Mutual Funds Is the Most Popular Long-Term Investment in India

Currently, equity mutual funds through SIP (Systematic Investment Plan) are the most popular long-term investment vehicle in India.

The reason is simple.

SIP makes investing:

- Easy to start

- Affordable

- Disciplined

- Suitable for salaried individuals

You don’t need lakhs to begin.

Even ₹1,000 per month is enough to start building long-term wealth.

If you are just starting your journey, you can read:

- How to Invest ₹1,000 Per Month – Ideal for beginners who want to start small and build discipline.

- How to Invest ₹5,000 Per Month – A practical strategy for early-stage investors.

- How to Invest ₹10,000 Per Month – Balanced portfolio allocation for salaried professionals.

- How to Invest ₹20,000 Per Month – Suitable for mid-income earners aiming for faster wealth creation.

- How to Invest ₹30,000 Per Month – Aggressive growth approach with diversification.

- How to Invest ₹50,000 Per Month – Advanced allocation strategy for serious long-term investors.

These guides help you move from theory to action.

Instead of wondering where to invest money in India for long term, you can directly choose the plan based on your monthly investment capacity.

That is how structured investing works.

Frequently Asked Questions (FAQs)

1. When should you focus on long-term investments over short-term investments?

You should focus on long-term investments when your financial goal is more than 5 years away.

Long-term investing is suitable for:

- Retirement planning

- Child’s education

- Wealth creation

- Financial independence

If your goal is within 1–3 years, capital safety is more important than growth. In that case, short-term debt instruments are better.

For goals beyond 5 years, equity-oriented investments become more effective because time reduces volatility and increases compounding benefits.

2. What is the most popular long-term investment in India?

Currently, equity mutual funds through SIP (Systematic Investment Plan) are the most popular long-term investment option in India.

They are popular because:

- You can start with as little as ₹500–₹1,000 per month

- Professional fund management

- Suitable for salaried individuals

- Historically better long-term growth compared to traditional savings products

SIP investing has become the preferred method for long-term wealth creation.

3. Which is the most popular low-risk investment plan with good returns?

For low-risk long-term investing in India, popular options include:

- Public Provident Fund (PPF)

- Employee Provident Fund (EPF)

- National Pension System (NPS) (low equity allocation option)

- Senior Citizen Savings Scheme (for retirees)

These options provide stability and moderate returns.

However, low risk usually means lower return compared to equity investments.

4. Which long-term investment plan gives the highest return?

Historically, equity investments (direct stocks and equity mutual funds) have provided the highest long-term returns in India.

However:

- Returns are not guaranteed

- Short-term volatility is high

- Emotional discipline is required

Higher return potential always comes with higher risk.

For most investors, diversified equity mutual funds provide a better balance between return and risk.

5. How much should I invest monthly for long-term wealth creation?

The amount depends on:

- Your income

- Your financial goals

- Your retirement target

- Your time horizon

As a basic rule, try to invest at least 20–30% of your monthly income.

You can calculate your required SIP using your retirement corpus target and expected return assumptions.

Use your SIP calculator here: SIP & Lumpsum Calculator

6. Is Fixed Deposit good for long-term investment?

Fixed Deposits are safe but generally do not beat inflation over long periods.

They are suitable for:

- Emergency funds

- Short-term goals

- Risk-averse investors

For long-term wealth creation (10+ years), equity-oriented investments are usually more effective.

7. Who should consider long-term investing?

Long-term investing is suitable for:

- Salaried professionals

- Business owners

- Young earners in their 20s and 30s

- Parents planning for education

- Anyone planning retirement

If your goal is long-term financial stability, disciplined investing over decades is essential.

Disclaimer

The information provided in this article is for educational and informational purposes only. It does not constitute financial, investment, tax, or legal advice.

Investment returns are not guaranteed, and past performance does not indicate future results. All investments, especially equity-related investments, are subject to market risks. Please read all scheme-related documents carefully before investing.

Your financial situation, risk tolerance, income stability, and goals may differ from others. It is advisable to consult a qualified financial advisor or tax professional before making any investment decisions.

Finkari does not recommend any specific fund, stock, or financial product. The examples and allocations mentioned are for illustration purposes only.