If you can invest ₹5,000 per month, you’re already doing better than most people.

At this stage, you may not feel “rich” or financially secure yet. Your salary might still be growing, expenses may be high, and savings may feel limited. But the fact that you’re thinking about investing ₹5,000 every month means you’ve taken the most important step — starting.

Many beginners believe small monthly investments don’t make a big difference.

But in reality, consistency matters far more than amount.

Someone who invests ₹5,000 every month for the next 15–20 years will often build more wealth than someone who waits for the “perfect time” or larger salary to start investing.

That’s because wealth is built through discipline, not big one-time decisions. Small, regular investments combined with time can quietly grow into something meaningful.

So the real question is not whether ₹5,000 is enough.

The real question is:

How should you invest ₹5,000 per month to build long-term wealth in India?

Many people get confused here.

There are too many options:

Mutual funds, SIPs, FDs, gold, stocks, different apps and advice from different people.

Instead of chasing the “best” investment, what you need is a clear and simple structure — a system you can follow every month without stress or confusion.

In this detailed beginner-friendly guide, you’ll learn:

- How to invest ₹5,000 per month step-by-step

- Best investment options for beginners

- Where exactly your ₹5,000 should go

- How much this amount can grow over time

- Mistakes to avoid

- How to increase investments as income grows

By the end of this guide, you’ll have a clear plan to invest ₹5,000 per month in a smart, practical, and stress-free way.

Let’s start by understanding what ₹5,000 per month can really do over time.

What ₹5,000 Per Month Really Means for Your Future

₹5,000 per month may not feel like a large amount today.

With rising expenses and lifestyle costs, it can even feel small. Many people delay investing because they believe they need a bigger salary or more savings to start.

But in investing, the amount matters less than two things:

Consistency

Time

Someone who invests ₹5,000 every month for 15–20 years can often build more wealth than someone who invests larger amounts occasionally but stops frequently.

Consistency builds momentum.

Time allows compounding to work.

When these two combine, even a modest monthly investment can grow into a meaningful corpus.

Here’s a simple example of how ₹5,000 per month can grow over time if invested in equity mutual funds with an average long-term return of around 12% annually.

| Investment Duration | Monthly Investment | Estimated Value |

|---|---|---|

| 5 Years | ₹5,000 | ₹4–4.5 Lakhs |

| 10 Years | ₹5,000 | ₹11–12 Lakhs |

| 15 Years | ₹5,000 | ₹25–30 Lakhs |

| 20 Years | ₹5,000 | ₹45–50 Lakhs |

These numbers are not guaranteed. Markets will go up and down. Some years will be slower, some stronger.

But historically, disciplined long-term investing has rewarded patient investors.

Over time, this monthly ₹5,000 can help you:

Build an emergency cushion

Create a long-term investment habit

Generate wealth for future goals

Move closer to financial independence

The goal is not to chase quick returns.

The goal is to stay consistent long enough for compounding to work in your favor.

Before deciding where this ₹5,000 should go every month, there is one important step to complete first.

Before You Invest ₹5,000 Per Month – Fix the Foundation First

Before deciding where to invest your ₹5,000 every month, it is important to make sure your financial basics are stable.

Many beginners start investing without building a strong foundation. Then when an emergency happens, they stop their SIP or withdraw investments early. This breaks consistency and reduces long-term wealth.

Investing works best when your finances feel calm and secure.

So before investing aggressively, make sure these three basics are in place.

1. Build a Small Emergency Fund

An emergency fund protects you from unexpected situations like job loss, medical expenses, or urgent travel.

You do not need a huge amount to start. Even saving 2–3 months of basic expenses in a separate savings account or liquid fund is enough in the beginning.

This ensures you don’t need to stop your investments during emergencies.

2. Get Basic Health Insurance

Medical expenses can destroy years of savings if you are not insured.

If your company provides health insurance, that’s good. But having a personal health insurance policy gives extra protection and long-term security.

When your health is financially protected, you can invest with more confidence.

3. Avoid High-Interest Debt

If you have credit card debt or personal loans with high interest, clear them before investing heavily.

Credit card interest can be 30–40% annually, which is much higher than any investment return. Paying off such debt gives a guaranteed return by saving interest.

Once high-interest debt is under control, investing becomes much more effective.

Why This Step Matters

When these basics are in place:

- You don’t panic during emergencies

- You don’t stop SIP midway

- You stay consistent with investments

- Your long-term wealth grows smoothly

You don’t need perfection here. Even a basic foundation is enough to start.

Once this is ready, you can confidently decide where your ₹5,000 per month should go and how to build a simple investment structure around it.

How to Invest ₹5,000 Per Month – Simple Allocation Strategy

When beginners start investing, they often try to find the perfect investment.

The perfect mutual fund.

The perfect stock.

The perfect timing.

But long-term wealth is not created by perfection. It is created by structure and consistency.

If you are investing ₹5,000 per month, you do not need complicated strategies or too many investment options. You just need a simple allocation that balances growth and stability.

For most beginners, a structure like this works well.

| Investment Type | Monthly Amount | Purpose |

|---|---|---|

| Equity Mutual Fund (Index or Flexi Cap) | ₹3,000 | Long-term wealth growth |

| Second Mutual Fund or Index Fund | ₹1,000 | Diversification |

| Gold ETF or Gold Fund | ₹500 | Stability and hedge |

| Liquid Fund or Savings | ₹500 | Emergency flexibility |

This allocation keeps things simple and practical.

Most of your money goes toward long-term growth through equity mutual funds. A small portion goes into gold for stability, and a small portion remains accessible for flexibility.

You can adjust this slightly based on your comfort with risk. The goal is not to create a perfect portfolio but to create a system you can follow every month without stress.

The best investment plan is the one you can continue for years.

Consistency matters more than complexity.

Why Mutual Funds Should Form the Core of Your ₹5,000 Investment

If you invest ₹5,000 per month, mutual funds should usually form the core of your portfolio.

Not because they are trending.

But because they make investing simple, diversified, and practical for beginners.

When you invest in individual stocks, you need time to research companies, track markets, and handle volatility. Most beginners either don’t have the time or the experience for this.

Mutual funds solve this problem.

They pool money from many investors and invest across multiple companies. This diversification reduces risk and makes long-term investing smoother.

With a monthly investment of ₹5,000, mutual funds allow you to:

- Start with a small amount

- Invest consistently through SIP

- Avoid timing the market

- Benefit from long-term compounding

- Stay diversified without large capital

You do not need to select too many funds. In fact, keeping things simple usually works better.

A basic structure like this is enough for most beginners:

- One index fund (Nifty 50 or Sensex)

- One flexi-cap or large-cap fund

That’s it.

You don’t need five different funds.

You don’t need constant switching.

You don’t need to check markets daily.

Simple and consistent investing usually creates better long-term results than complex strategies.

Over time, as your income increases, you can increase your SIP amount or add new investments. But in the beginning, keeping your portfolio simple makes it easier to stay consistent.

And consistency is what ultimately builds wealth.

How Much Can ₹5,000 Per Month Grow Over Time?

Most people underestimate what consistent investing can do.

₹5,000 per month may not feel life-changing today. But when this amount is invested regularly and given enough time, the results can become meaningful.

Let’s look at this realistically.

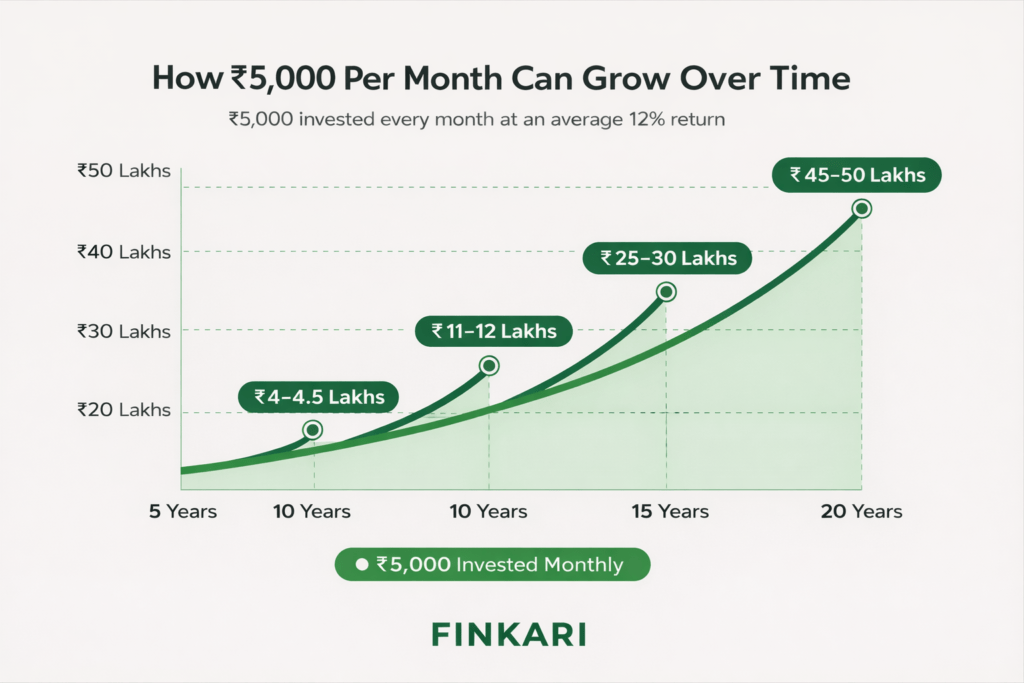

Assuming an average long-term return of around 12 percent annually from equity mutual funds, here’s how ₹5,000 per month can grow.

After 5 Years

Total invested: ₹3 lakhs

Estimated value: ₹4–4.5 lakhs

At this stage, compounding is just starting. Growth feels slow, and many investors lose patience here. But this is where discipline matters most.

After 10 Years

Total invested: ₹6 lakhs

Estimated value: ₹11–12 lakhs

Now compounding becomes visible. Your money is starting to work harder than your monthly contribution.

After 15 Years

Total invested: ₹9 lakhs

Estimated value: ₹25–30 lakhs

This is where the real power of long-term investing becomes clear.

After 20 Years

Total invested: ₹12 lakhs

Estimated value: ₹45–50 lakhs

You invested ₹5,000 per month.

Time and consistency did the heavy lifting.

Why Time Matters More Than Amount

Many people delay investing because they think ₹5,000 is too small.

They wait for a salary increase.

They wait for a better time.

But in investing, starting early matters more than starting big.

Someone who starts investing ₹5,000 today and increases slowly over time will usually build more wealth than someone who waits 8–10 years and then starts with a larger amount.

Time multiplies money.

Consistency multiplies time.

That is the simple formula behind long-term wealth creation.

Also, read our article on How to invest ₹10,000 per month

How to Turn ₹5,000 Per Month Into ₹15,000 or More Over Time

₹5,000 per month is a strong starting point.

But it should not remain ₹5,000 forever.

The real acceleration in wealth building happens when your investments grow along with your income. Many investors increase their lifestyle every year but forget to increase their investments.

If you continue investing only ₹5,000 per month for the next 20 years, you will still build decent wealth. But if you increase your SIP gradually as your salary grows, the results become dramatically better.

This approach is called a step-up investment strategy.

Step 1 – Increase SIP When Income Increases

Whenever your salary increases, try to increase your SIP by at least 10 to 20 percent.

Even a small increase of ₹500 or ₹1,000 every year can make a big difference over long periods.

For example:

Year 1 – ₹5,000 per month

Year 2 – ₹6,000 per month

Year 3 – ₹7,000 per month

Year 5 – ₹10,000 per month

Year 8 – ₹15,000 per month

Without feeling sudden pressure, your investment capacity grows naturally with your income.

What Difference Does This Make?

Let’s keep this simple.

If you invest ₹5,000 per month for 20 years at around 12 percent average return, you may build around ₹45–50 lakhs.

But if you increase your SIP by just 10 percent every year, the final amount can grow significantly higher and may even cross ₹70–80 lakhs over long periods depending on consistency.

The difference is not intelligence or timing.

The difference is discipline and gradual increase.

When Should You Increase Investments Faster?

There are certain situations where you should strongly consider increasing your investments:

- After a salary hike

- After a job change with higher income

- After clearing a major loan

- After receiving bonuses

- When expenses are under control

Most people increase lifestyle first and investments later.

Successful investors do the opposite.

They increase investments first.

Lifestyle adjusts automatically.

The Real Wealth Formula

Start with ₹5,000.

Stay consistent.

Increase slowly every year.

Stay invested for the long term.

You do not need complicated strategies.

Consistency plus time plus gradual increase creates long-term financial security.

Biggest Mistakes to Avoid While Investing ₹5,000 Per Month

Investing ₹5,000 per month sounds simple.

But small mistakes can quietly reduce your long-term wealth. Most people do not fail because investments are bad. They fail because their behavior becomes inconsistent.

If you avoid the mistakes below, your chances of building meaningful wealth increase significantly.

1. Starting and Stopping Frequently

Some months you invest.

Some months you skip.

Some months you stop completely.

This breaks compounding.

Wealth is built through consistency, not intensity. Even if the amount feels small, try to maintain your monthly investment habit unless absolutely necessary.

Consistency matters more than amount.

2. Expecting Quick Results

Many beginners expect strong returns within one or two years.

But real compounding becomes visible after five to seven years. Serious wealth usually appears after ten or more years of disciplined investing.

If expectations are unrealistic, investors lose patience and stop too early.

Investing is a long-term process. Patience is required.

3. Changing Funds Too Often

Switching mutual funds frequently rarely improves results.

A fund may underperform for a short period. Markets may go through cycles. But constantly changing funds creates confusion and interrupts long-term growth.

Choose good funds.

Review once a year.

Avoid frequent changes.

4. Not Increasing Investments Over Time

This is one of the biggest silent mistakes.

Income increases.

Expenses increase.

But investments remain the same.

If your SIP stays ₹5,000 for many years despite salary growth, wealth creation slows down. Increase your investment gradually whenever your income grows.

5. Panic During Market Falls

Markets will fall sometimes.

There may be temporary declines of 10 percent, 20 percent, or even more. This is normal.

Panic selling during market corrections permanently damages long-term wealth. If your investment horizon is long and your allocation is sensible, market volatility is temporary.

Calm investors build wealth.

Emotional investors interrupt it.

Avoiding these mistakes is often more important than finding the perfect investment plan.

Final Thoughts – Is ₹5,000 Per Month Enough to Build Wealth?

Yes, ₹5,000 per month is enough to start building real wealth.

Not because the amount is huge.

But because the habit is powerful.

Most people underestimate small beginnings. They think meaningful wealth requires large capital. In reality, wealth is built through consistent monthly investing, patience, and gradual growth.

If you invest ₹5,000 per month wisely:

- You build financial discipline

- You create long-term investment habits

- You benefit from compounding

- You reduce financial stress over time

The key is not to overthink.

You do not need complicated strategies.

You do not need to track markets daily.

You do not need perfect timing.

You need a simple structure you can follow every month without stress.

Start with ₹5,000.

Stay consistent.

Increase when income grows.

Give your investments time to work.

Over the years, this simple approach can quietly transform your financial future.

Not overnight.

But steadily.

And steady wealth is the kind that lasts.

1 thought on “How to Invest ₹5,000 Per Month in India (2026 Guide)”